Topic 7: INSURANCE: SLUGGISH OVERSIGHT

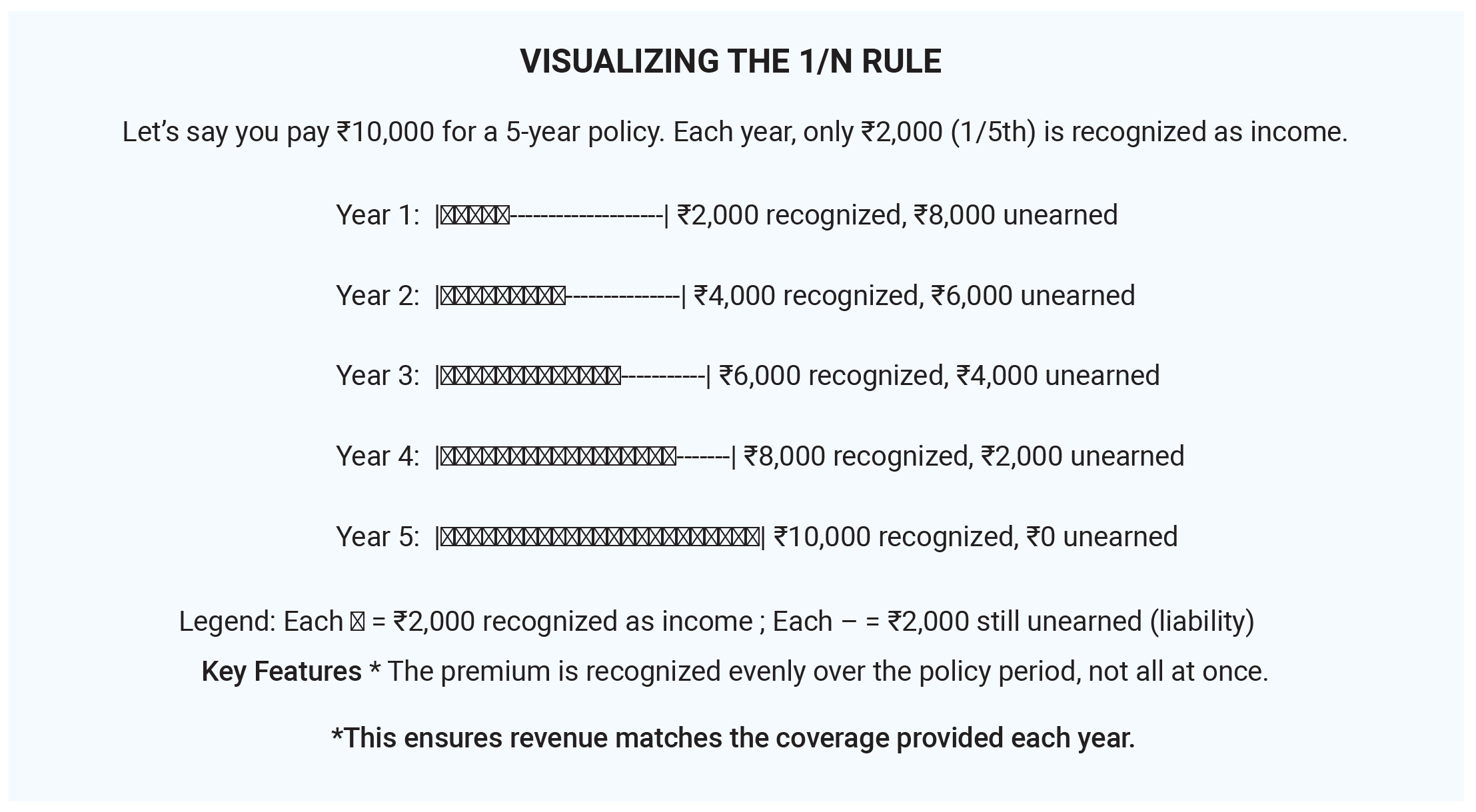

April 2025 was a defining month for India’s insurance industry—marked by a stark slowdown in growth, profitability concerns, and persistent consumer awareness challenges. Yet, the sector also showed signs of evolution, with bold regulatory reforms and foreign investment plans pointing to a more dynamic future. The non-life insurance segment witnessed a sharp deceleration, with overall industry growth halving in FY25. A combination of regulatory adjustments—most notably the new "1/n rule" on commission payouts—along with tepid vehicle sales and subdued commercial demand contributed to this downturn. Public sector insurers managed to post modest growth of 5.5% year-on-year in March, while private players reported a decline in premium collections.

Health insurance, which had been a key growth driver in recent years, led the slump. The sector's overall non-life premium growth fell to just 6.2% in FY25, down from 12.8% in FY24. Industry experts attributed this pullback to the broader economic slowdown and rising premiums, which strained consumer affordability. The profitability outlook remained muted for both life and general insurers. Life insurers grappled with margin compression as consumers increasingly moved away from high-margin products such as traditional endowment plans. On the general insurance front, high claim ratios—particularly in health and motor segments—strained balance sheets. Analysts predict subdued Q4 FY25 earnings for both segments. A nationwide survey revealed that nearly half of Indian consumers are still unaware of term insurance, highlighting the persistent financial literacy gap. This is despite the term insurance segment growing 18% in FY24, indicating that awareness remains a critical bottleneck for deeper market penetration. April also saw the groundwork laid for significant structural reforms. The government’s proposal to allow 100% foreign direct investment (FDI) in the insurance sector stirred global interest, with expectations of increased capital inflows, innovation, and expanded market coverage. If implemented, this reform could mark a turning point in India's insurance journey. Meanwhile, reinsurance developments gained momentum. International reinsurer Peak Re secured a license to operate in GIFT City, underlining India’s aspirations to position itself as a reinsurance hub for the broader Asia-Pacific region. Travel insurance saw an uptick in demand, driven by a post-pandemic surge in international travel, particularly among Gen Z consumers. In parallel, insurers began exploring customised solutions tailored for high-risk and emerging industries, including nuclear energy and marine logistics, to better serve the evolving risk landscape. While April 2025 highlighted the Indian insurance industry’s near-term struggles—from slowing growth to profitability constraints—it also showcased its potential for transformation. With major regulatory shifts, rising investor interest, and evolving customer needs, the sector stands at the threshold of a new chapter—one defined by innovation, inclusion, and global integration.